We don’t have to tell you that canceling a timeshare is a difficult feat to accomplish. If you’ve been at the process for a while, you’re already aware that timeshare companies want their customers locked into ownership for life. They don’t want you to be able to just walk away if you decide ownership isn’t for you anymore.

But what happens if you find yourself periodically skipping out on timeshare loan payments? Or if your developer reclaims your property? Fortunately, there is a silver lining — your loan will be pardoned, and you will no longer be a timeshare owner. However, when you are finally free, their parting gift will be a 1099 C or 1099 A timeshare form.

Indeed, the release and closure of a timeshare loan will result in a 1099 form. And so will foreclosure. Of course, no homeowner wants their personal property foreclosed on. But some people can find themselves in a position where there seems to be no other option. They’ve already tried canceling the timeshare with their developer and selling their property on the online resale market. But since both of those paths are rarely successful, they have to choose between paying off their mortgage on their primary home and paying off their timeshare loan.

Whether you’ve been released from your timeshare loan or forced into foreclosure because you’re trying to avoid the repossession of your main home, you’re going to receive a 1099 C or 1099 A form. If this is the situation you’ve found yourself in, here’s how to deal with receiving either of these IRS forms from your timeshare developer.

Before getting into what you should do when you receive one of these forms, let’s differentiate form 1099-A from form 1099-C. The 1099-A tax form is utilized by loan lenders to report an abandonment of secured property. In simpler terms, it’s issued when someone stops paying the loan on their property and is thus foreclosed on. 1099-A forms aren’t just for timeshare owners. They can apply to any type of unpaid real estate, regardless of whether it’s a business property or for personal use.

The 1099-A timeshare tax form will always include information such as your tax identification number, the date you acquired your timeshare, the fair market value of your property, and the outstanding balance on your loan. Your lender must apply this form to the tax year in which the foreclosure took place. If the amount you owe is more than the fair market value, you will receive a cancellation of debt form, which is known as the 1099-C form.

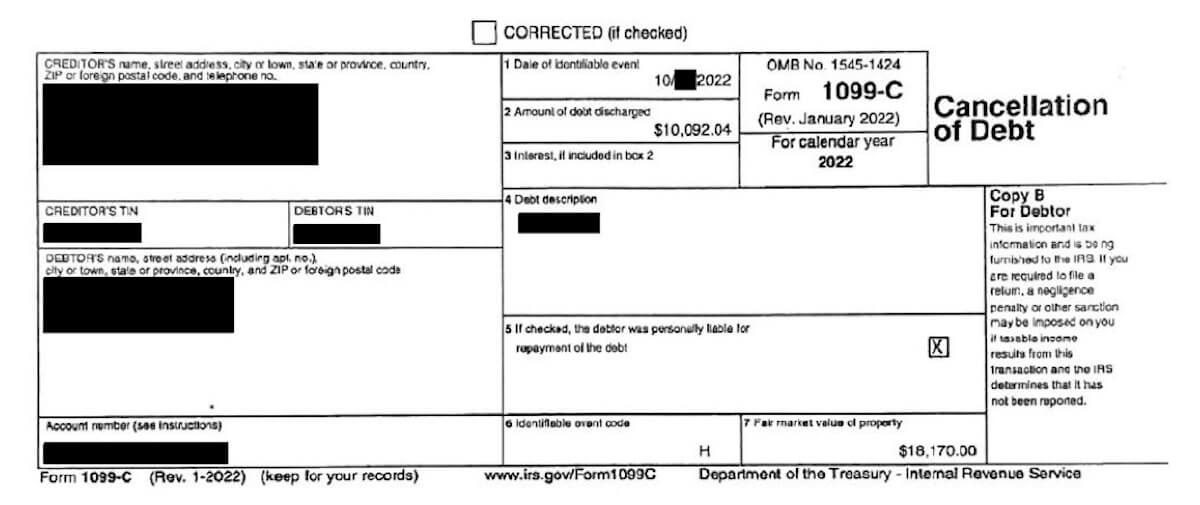

A tax 1099-C form is used by lenders to report canceled debt to the IRS. A copy of this form is then given to the loan borrower to inform them about how much money they no longer owe on their loan. This canceled debt must then be reported as taxable income, meaning that a small percentage of it must be paid off to the government.

How does income reporting work in relation to debt forgiveness and timeshare fair market value? In the event that the sum of your debt forgiveness amounted to $25,000, and the fair market value of your timeshare was $20,000, you would need to report $5,000 as taxable income. However, if both your loan forgiveness and timeshare fair market value were $12,000, then you would not have any taxable income to report.

There are a few reasons why you would no longer be responsible for the repayment of the debt on your loan:

Though these situations may make it seem like you’re off the hook, they’re still linked to the unfortunate occurrence of a timeshare foreclosure. Foreclosures can cause levies to be placed on your bank accounts, affect your ability to apply for credit cards, make it difficult to purchase property in the future, and drastically decrease your credit score.

This isn’t the ideal method for exiting timeshare ownership. But if this is where you’ve found yourself, you must know how to navigate the 1099-A and 1099-C timeshare tax process.

Any timeshare owner who receives one or both of these forms should be prepared for a grueling tax season. So the best thing you can do in this situation is make sure you have all the information needed to come away from this foreclosure mostly unscathed. Here are a few tips for managing the 1099-A timeshare tax process.

This may sound obvious, but overlooking this step can greatly impact the amount of taxable income you have to report. Ensure that the fair market value listed on the 1099-A is realistic by comparing it to similar timeshares on the online resale market. You may also want to look up tax assessments for your timeshare property if they’re available. Finding out the property tax on your timeshare can help determine how accurate the fair market value listed is.

Handling a foreclosure for the first time is no easy feat. Neither is dealing with anything related to timeshare cancellation. So even if you’re accustomed to doing taxes on your own, it may be time to hire a tax professional. A CPA with experience in real estate and foreclosures can help you navigate through the filing process by pointing out tax liabilities and protecting you from potential scams.

If you received both the 1099-C and 1099-A timeshare tax forms, file your taxes as soon as possible. This prevents you from paying late penalties and helps determine if there are more forms you need to fill out. Form 982, for example, will need to be filled out if the reason for your debt cancellation was bankruptcy. In this case, you would be eligible for an income exclusion, which could save you some money.

No one wants to be pulled back into the drama of timeshare ownership after they’ve finally escaped it. But we all know that timeshare developers have highly effective ways of nickel-and-diming their customers.

It’s not unlikely that a timeshare company would make false claims about unpaid fees that you owe them, like termination-of-contract fees or end-of-membership fees. If you keep track of all the tax forms, loan statements, purchase documents, and email correspondence between you and your developer, they’ll have no way of further embezzling you.

Getting the 1099-C or 1099-A timeshare tax form is a bit of a double-edged sword. It does mean that you are out of your timeshare contract, which can be a huge relief for anyone who has struggled to break free from the burden of annual maintenance fees. But it also means you have to deal with the repercussions of foreclosure.

Beyond having to file tedious tax forms, foreclosures can have devastating effects on your life and financial well-being. So if you’re looking to get out of your timeshare contract without ruining your credit, it’s best to avoid foreclosure at all costs. Unfortunately, developers rarely allow customers to cancel their timeshares. On top of that, the resale market is outrageously competitive and highly unsuccessful. Finding a legitimate and effective method for timeshare cancellation can clearly be challenging for many owners.

Luckily, Centerstone Group can make this goal attainable. Centerstone Group is a full-service advocacy group with overwhelmingly positive reviews and a 4.78 star rating with the Better Business Bureau. Our team of timeshare industry experts can resolve your timeshare contract issues at a fast, affordable rate, saving you tons of time and money. If you want to avoid a 1099-A timeshare tax crisis, call us for your free first consultation.